Among economists, there is near unanimous consensus that a necessary component of any portfolio of policies to address climate change includes carbon pricing. However, this sentiment is not shared nearly as widely among policymakers and the general public. Much of the political opposition to carbon pricing and carbon taxes in particular is driven by vested interests in fossil fuel production and the obfuscation of scientific facts. However, some of the opposition is driven by confusion or misunderstanding of the policy impacts. This paper addresses those misunderstandings and focuses in on five myths: 1) that a carbon price will hurt economic growth; 2) that carbon pricing will kill jobs; 3) that a carbon tax and cap and trade program have the same economic impacts; 4) that we can’t achieve carbon reduction targets with a carbon tax; and 5) that carbon pricing is regressive. I find that all five of these statements are false.

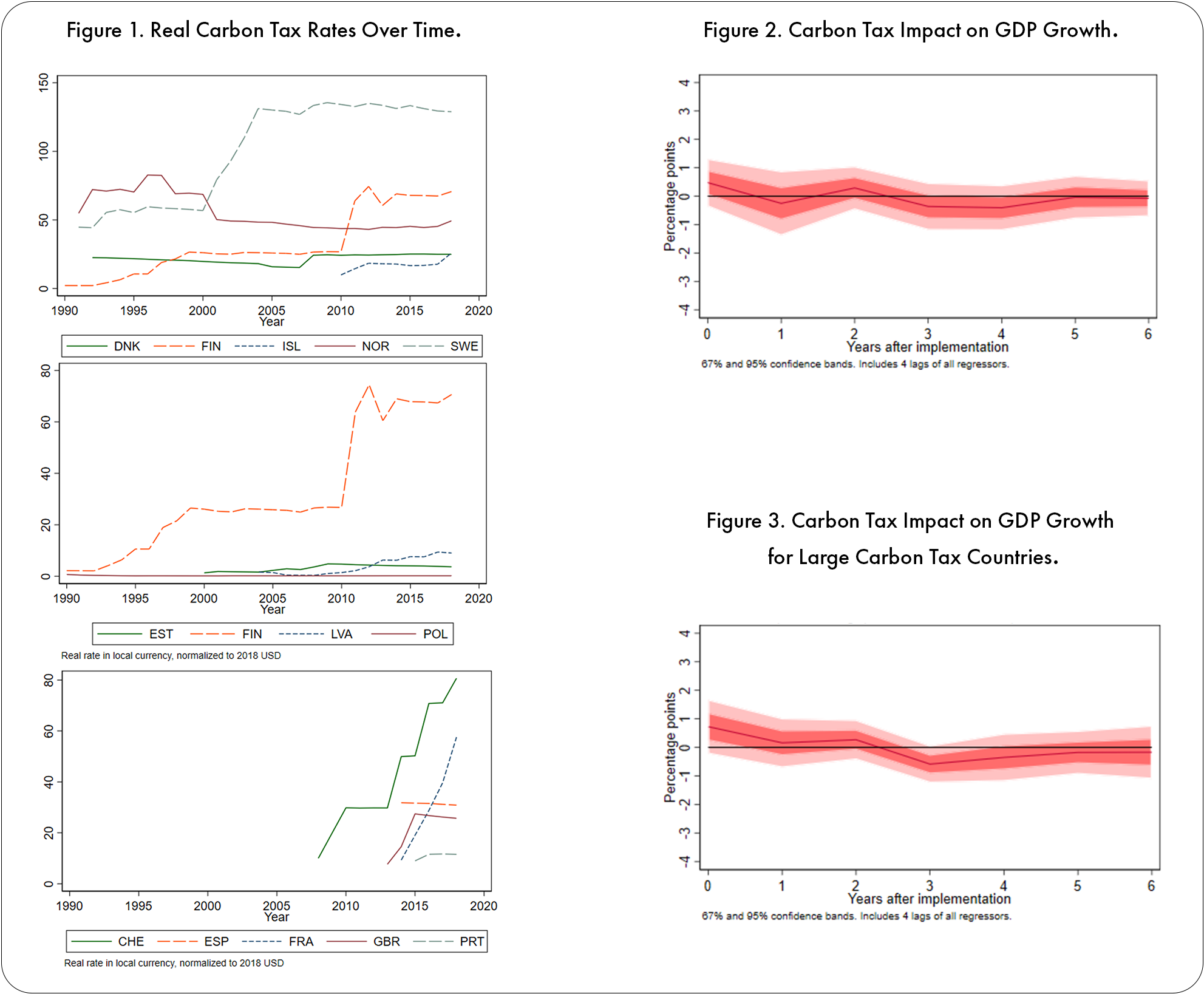

I begin by addressing the first myth, that carbon pricing will hurt economic growth. Undeniably, any program to reduce pollution will have economic costs. But how large are the costs? One way to assess this is to look at the impact of existing carbon taxes on economic growth. I analyze the results of a paper produced by Metcalf and Stock (forthcoming) in which they examine carbon taxes employed in 15 European countries. They estimate the dynamic effect on GDP growth of the unexpected component of the carbon tax using a local projection method. Their study produces impulse response functions (IRF’s) for a counterfactual of a one-time permanent increase in the carbon tax by $40, for a tax that covers 30% of the country’s emissions. They find no significant impact on GDP growth, either in a positive or a negative direction (see figures below), which is consistent with existing theory that long run GDP growth rates are driven more by fundamentals than by policy variables such as tax rates. I conclude that, based on the burgeoning literature on the economic impact of carbon taxes, there is little evidence that carbon taxation has a significant adverse effect on economic growth.

I turn next to the second carbon pricing myth – that carbon pricing is a job killer. Once one accepts the view that carbon pricing does not hurt economic growth, it is not surprising to learn that it doesn’t adversely impact overall employment either. The results from Metcalf and Stock (2020, forthcoming) support this view. Similarly, an analysis of the employment effects of the British Columbia carbon tax by Yamazaki (2017) found modest positive impacts on employment. While aggregate impacts were small, he found significant job shifting from carbon intensive to non-carbon intensive sectors. A fall in carbon intensive sector employment is not surprising. That the tax does this without affecting overall employment is encouraging, though the analyses to date have not addressed the transitional costs of making the shift.

A third myth is that carbon taxes and cap and trade programs are equivalent. Carbon pricing entails raising the marginal cost of producing goods that burn fossil fuels in their production, therefore aligning private and social costs. Cap and trade programs and carbon taxes are dual instruments. However, important differences between the two carbon pricing systems remain. The two systems differ in three important ways. First, since a cap and trade system fixes emissions, prices fluctuate with economic conditions. These fluctuations complicate life for businesses focused on long-lived capital-intensive project investments. A carbon tax provides price certainty that provides some reassurance for project planning. Second, most countries have well-functioning tax collection systems and already impose fuel excise taxes. Thus, imposing a carbon tax involves little incremental investment in administrative systems. In contrast, cap and trade systems generally requires an entirely new administrative agency to create and track allowances, hold auctions, and develop rules to prevent fraud and abuse. The third and by far the most important difference is in how the two carbon pricing systems interact with other carbon reduction policies. Complementary policies tend to relax binding caps. Therefore, depressed allowance prices in emission trading systems may help explain why cap and trade system tend to have lower prices than the tax rates of carbon tax systems.

I also refute myth 4: that carbon taxes are incompatible with emissions reduction targets. In Metcalf (2009), I sketched out an initial way to construct a carbon tax to achieve emission reduction goals. I followed that up in Metcalf (2020) with a more detailed proposal for a U.S. Emissions Assurance Mechanism (EAM) to include as part of carbon tax legislation. The EAM proposal creates a target emission reduction focusing on cumulative emission reductions relative to the baseline over the fifteen-year period. This reflects the fact that greenhouse gas emissions are a stock rather than a flow pollutant. Having a target based on a particular future year means many different emission pathways with different cumulative emissions could be consistent with that target. While this approach does not guarantee that emission reduction targets are hit, it provides some assurance that targets will be met. Just as one can add carbon tax elements to a cap and trade program to control prices, one can add cap and trade elements to a carbon tax to provide greater assurance of hitting desired emission reduction targets. Therefore, a carbon tax can clearly be made to support political commitments to emission reduction goals.

I conclude by challenging the fifth myth: that carbon pricing is regressive. Carbon pricing is, to a large extent, a tax on energy consumption. It has long been understood that household spending on energy is a larger fraction of income for lower income households than for higher income households. Thus, the logic goes, carbon pricing is regressive since it raises the cost of energy which is a higher share of household budgets for low-income households. What this ignores is the fact that taxes have impacts on household income sources (wages, transfers, and capital income). Economists refer to the former as “uses side impacts” and the latter as “sources side impacts.” We can decompose the distributional impacts of a tax reform into source and use side influences. I provide a theoretical framework to justify the work of Rausch et al. (2011). Their paper provides an example of such a decomposition by analyzing a carbon pricing policy where the revenue from the policy is distributed in a way that does not enter household utility. Their results suggest that the conventional view of a carbon tax as regressive must be re-examined, given the importance of source-side impacts. In fact, analyses focusing on a U.S. carbon tax suggest the tax would be progressive even before considering how to rebate the revenue.

References

Metcalf, Gilbert E. 2009. “Cost Containment in Climate Change Policy: Alternative Approaches to Mitigating Price Volatility.” Virginia Tax Review, 29, 381-405.

Metcalf, Gilbert E. 2020. “An Emissions Assurance Mechanism: Adding Environmental Certainty to a Carbon Tax.” Review of Environmental Economics and Policy, 14(1), 114-130.

Metcalf, Gilbert E. and James H. Stock. 2020. “Measuring the Macroeconomic Impacts of Carbon Taxes.” American Economic Association: Papers and Proceedings, 110(May), 101-106.

Metcalf, Gilbert E. and James H. Stock. forthcoming. “The Macroeconomic Impact of Europe’s Carbon Taxes.” American Economic Journal: Macroeconomics.

Rausch, Sebastian; Gilbert E. Metcalf and John M. Reilly. 2011. “Distributional Impacts of Carbon Pricing: A General Equilibrium Approach with Micro-Data for Households.” Energy Economics, 33, S20-S33.

Yamazaki, Akio. 2017. “Jobs and Climate Policy: Evidence from British Columbia’s Revenue-Neutral Carbon Tax.” Journal of Environmental Economics and Management, 83, 197-216.

Further Reading: CEEPR WP 2022-016

About The Authors

|

Gilbert E. Metcalf is a Visiting Professor at the Sloan School of Management and CEEPR at MIT. He is also the John DiBiaggio Professor of Citizenship and Public Service and a Professor of Economics at Tufts University. Metcalf’s primary research area is applied public finance with particular interests in taxation, energy, and environmental economics. His current research focuses on policy evaluation and design in the area of energy and climate change. During 2011 and 2012, he served as the Deputy Assistant Secretary for Environment and Energy at the U.S. Department of Treasury where he was the founding U.S. Board Member for the UN based Green Climate Fund. Metcalf received a B.A. in Mathematics from Amherst College, an M.S. in Agricultural and Resource Economics from the University of Massachusetts Amherst, and a Ph.D. in Economics from Harvard University. |