The U.S. government relies on investment tax credits to increase private-sector investment in renewable energy. Other governments, as well as some U.S. states, have also implemented carbon prices to incentivize low-carbon investments. How should such policies be designed? How do they compare?

This paper explores how the answers to such questions depend on the ability of investors in electricity markets to sign long-term contracts with consumers. In liberalized power systems, markets for long-term contracts are generally illiquid, which is also known as the missing market problem. As a result, investors in new generation or storage capacity can be exposed to unhedged risk. What do such risks imply for policy makers seeking to cost-effectively incentivize low-carbon investments?

To explore policy choices, we introduce a general, game theoretic framework for modeling climate policies. The model explicitly represents the decision making of a government acting in anticipation of electricity market behavior. The advantage of this approach is that it generalizes the choice of optimal climate policy. It can be used to analyze the design of a variety of policies in view of diverse government objectives. The more traditional approach – modeling an energy system subject to an emissions constraint – is a special case in the context of our model.

Our experiments consider a government that aims to meet a given CO2 target while maximizing social welfare. Risk-averse investors in new generation and storage capacity seek to maximize profit and consumers maximize consumer surplus. There is uncertainty about the overall electricity demand and the natural gas price. Importantly, investors and consumers lack the ability to engage in long-term electricity contracts. This missing market for risk drives a wedge between the optimal social welfare and the laissez-faire outcome from the electricity market. We refer to this as a “missing market” case, and compare it to a benchmark, “complete market” case, in which investors and consumers freely trade risk by engaging in long-term electricity contracts.

We compare two policies: investment tax credits for wind and solar and a carbon tax. In most of our experiments, we assume the government can use only one of these policy types. In each case, the government’s aim is to choose the level of the policy—the level of the tax or of the renewable subsidies—that will incentivize producer and consumer decisions that keep emissions below the target while maximizing social welfare.

Our results suggest that the completeness of long-term markets may be an important determinant of optimal policy design. We observe that optimal renewable subsidies and carbon taxes are higher when long-term markets are missing than when they are complete. Missing risk markets skew the investment mix away from renewables and storage in particular. To compensate, governments must strengthen climate policies, whether in the form of subsidies or a carbon tax.

To inform the choice between renewable investment tax credits and carbon pricing, we consider which of the two policies is more cost-effective. Cost-effectiveness is here defined as achieving a given emissions target at the lowest risk-adjusted power system cost, which is our measure of social welfare. We expect the carbon tax to be more cost-effective when markets are complete, but not necessarily in the missing markets case. The theory of second best suggests the optimal policy in an efficient economy (where risk trading is complete) may not be optimal in an economy subject to a market inefficiency (such as incomplete long-term contracting).

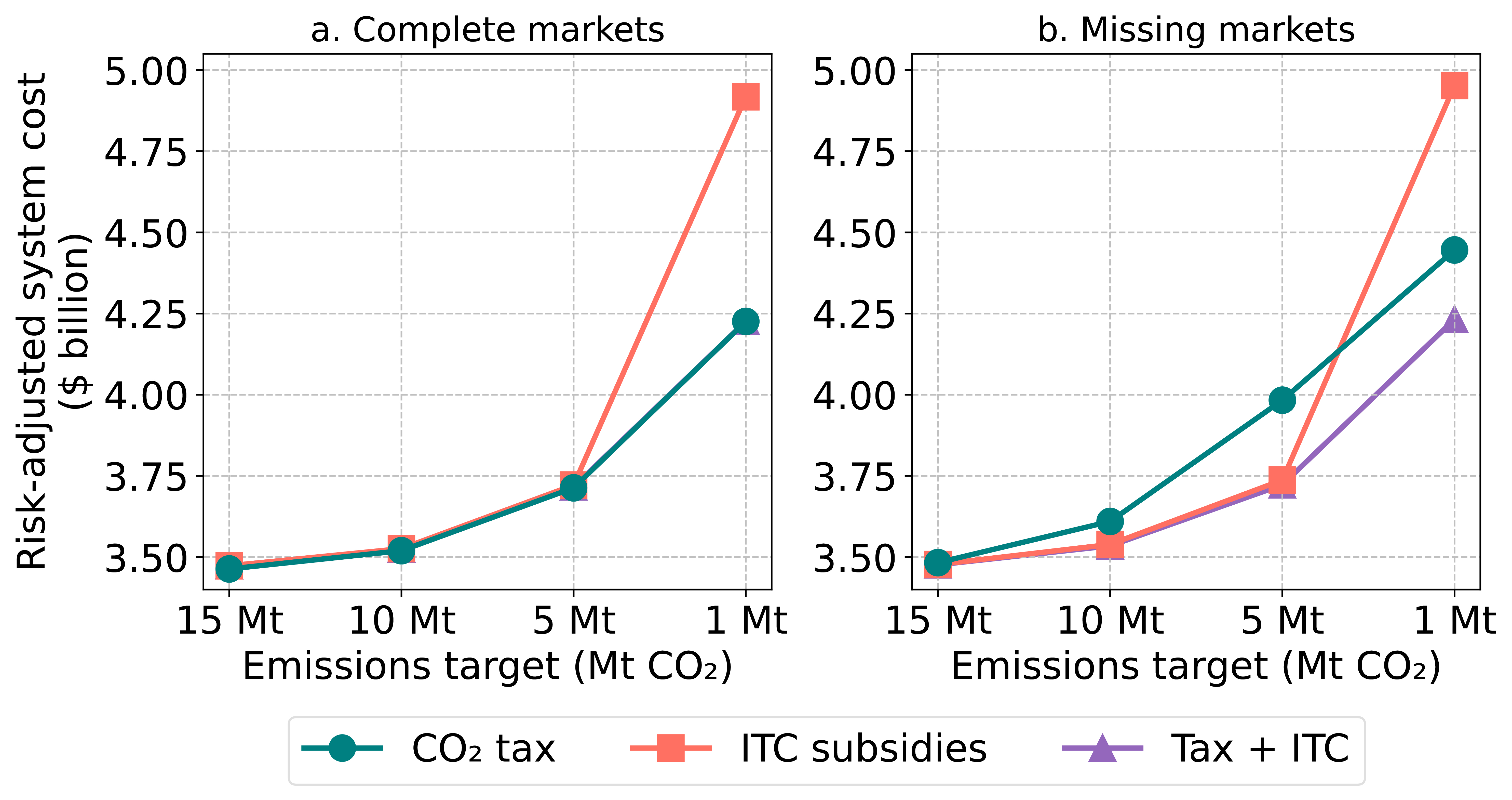

The figure below compares the cost-effectiveness of a carbon tax, wind and solar investment tax credits (labeled as ITC), and a policy mix, where the government can implement both policies at the same time.

Figure 1. Renewable investment tax credit (ITC) subsidies can reduce emissions at a lower risk-adjusted system cost vis-à-vis carbon pricing.

Source: Dimanchev et al., (2024)

The results suggest that the completeness of risk trading can influence the relative cost-effectiveness of subsidies and carbon pricing. When risk markets are complete (left panel in the figure), carbon pricing is always the most cost-effective policy instrument: it results in the lowest risk-adjusted system cost. This is in line with our expectations. However, when long-term contracting is missing (right panel), we observe renewable subsidies to be more cost-effective than carbon pricing in some cases.

This finding reflects a rarely considered channel through which climate policy can benefit the economy. When risk trading is incomplete, electricity producers and consumers are exposed to unhedged risk. Renewable subsidies can reduce risk by shifting investment decisions toward renewables, which reduces reliance on uncertain gas generation costs. While carbon pricing incentivizes renewable deployment, it also results in a greater reliance on gas with CCS relative to renewable subsidies.

A policy mix combining subsidies and pricing consistently achieves the lowest possible system cost across our experiments (as shown by the purple line in the figure). Subsidies on their own are more expensive than carbon pricing at the deepest decarbonization level (as shown by the right-most markers in the right panel of the figure). In this case, their economic cost vis-à-vis the carbon tax outweighs their risk-related benefits. By implementing the two policies together, a government can leverage the advantages of each policy.

These exploratory experiments suggest that climate policy choices may have to consider the ability of decision makers to trade risk. The incompleteness of long-term contracting in liberalized power markets also motivates the design of hybrid power markets that incorporate long-term contracting mechanisms.