As global economies increasingly shift towards electrification and low-carbon energy, understanding the impact of critical mineral price shocks compared to traditional oil price shocks has become crucial. Unlike oil price shocks, which affect the cost of utilizing existing capital, critical mineral price shocks influence the cost of creating new capital without altering the cost of existing capital. This paper compares the impacts of critical mineral price and oil price on an economy in a unified neoclassical growth model.

The New Commodity Frontier

The global economy is undergoing a fundamental structural pivot. As we transition from internal combustion to electrification, we are swapping a century-long dependence on oil for a new reliance on critical minerals like lithium, cobalt, and copper. This shift is not merely a change in resources but a change in strategic risk.

Critical mineral supply chains are significantly more concentrated than oil. China currently controls up to 80% of specific rare earth elements, exposing the energy transition to unique geopolitical bottlenecks. This vulnerability is compounded by shifting demand: by 2040, the IEA projects copper demand to surge by 50% while oil consumption is expected to fall by 25%. Consequently, policymakers must address a vital question: Do these new mineral price shocks pose the same recessionary threat as the historic oil shocks that triggered post-war downturns?

The Fundamental Distinction: Flow Inputs vs. Capital Formation

To answer this, we provide a unified neoclassical growth model that contrasts the impacts of oil and mineral price shocks. This framework reveals that the economic impact of a shock is determined by how a commodity enters the production cycle. We distinguish between these roles using a simple analogy: oil is the "gas in the tank," whereas minerals are the "steel and battery in the frame."

Oil as a Flow Input: Oil acts as a variable operating cost. It is required to utilize existing capital (e.g., fuel to run a car already on the road). Because it is consumed contemporaneously, oil-price spikes act like an adverse cost/productivity shock, immediately reducing output and welfare.

Minerals as Investment Components: Critical minerals are essential to capital formation. They affect the cost of creating new capital (e.g., the price of a new EV battery) without altering the productivity or operating cost of the existing capital stock.

Because minerals are embedded in investment goods—machinery, vehicles, and electrical equipment—their shocks propagate in a "slow but persistent" manner. While oil shocks hit the economy with immediate, fast-acting operational costs, mineral shocks act as an intertemporal drag on future capacity by raising the cost of investment.

Why Oil Price Shocks Remains the Greater Threat

Our findings demonstrate that both shocks lower output in the long run, but oil price increases are systematically more contractionary and damaging to aggregate welfare.

Key Comparative Impacts:

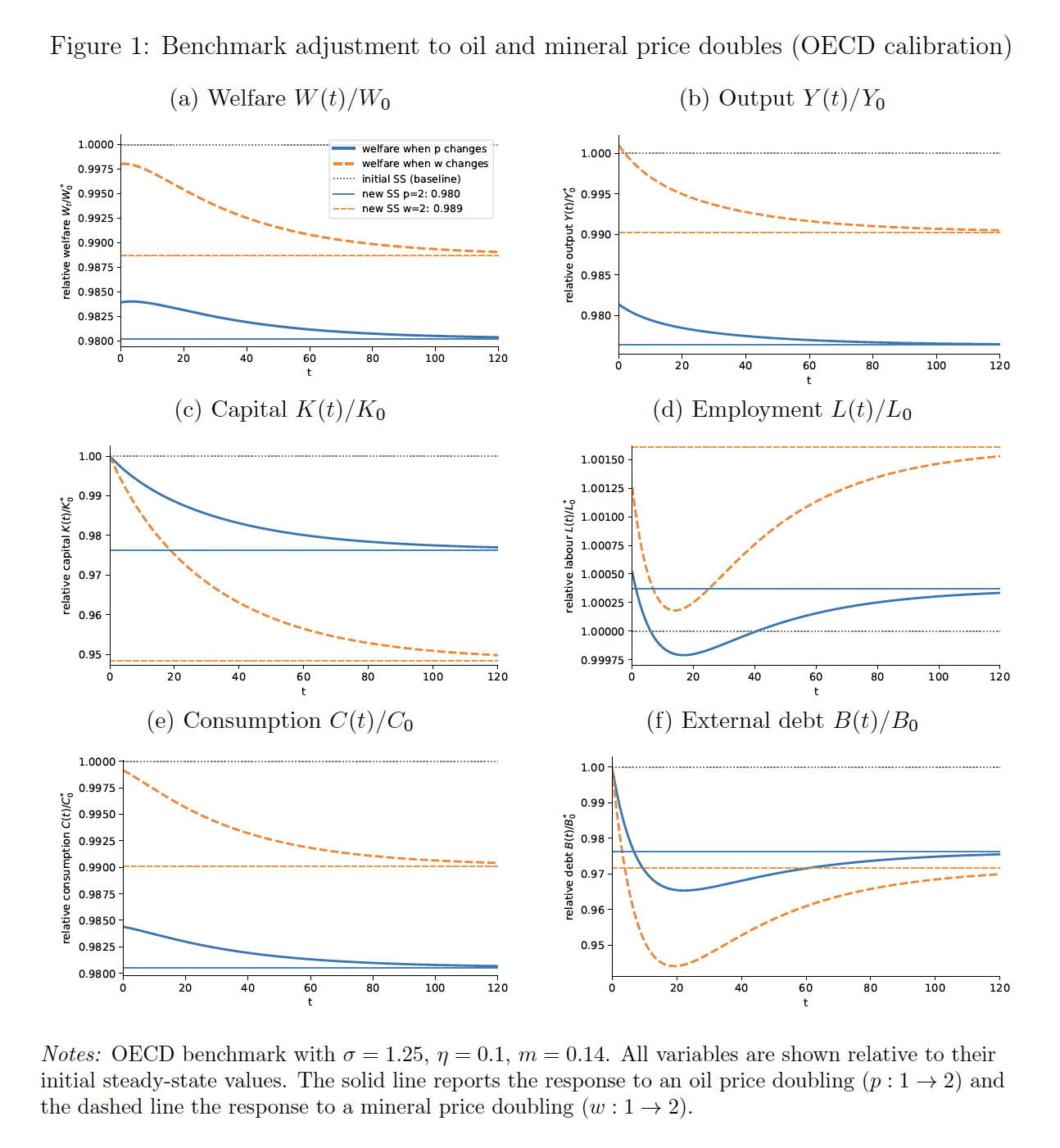

Output and Welfare: Our results show that oil shocks are more damaging. As shown in Figure 1 (Benchmark Adjustment), a doubling of oil prices (solid blue line) produces a deeper, more immediate collapse in welfare and output compared to a mineral doubling (dashed orange line).

Short-Term "Blips" vs. Long-Run Decline: While oil shocks cause an immediate drop, mineral price doublings can actually produce a "small positive blip" in output on impact (approximately 0.43% in certain scenarios) before gradually drifting into a milder long-run decline.

Capital Contraction: Mineral shocks generate a sharper contraction in capital stocks than oil shocks. Because minerals directly hit investment costs, firms cut new capital formation more aggressively.

Labor Dynamics and the Wealth Effect: Surprisingly, mineral shocks can increase long-run employment. We find this is driven by a two-fold mechanism: firms substitute labor for expensive capital, and households supply more labor to reconstruct their balance sheets and offset the erosion of net foreign wealth.

Policy Implications: Shifting the Stabilization Toolkit

Our model assumes prices adjust quickly. Mineral shocks mainly hit investment and foreign borrowing. Demand-side stimulus plays a smaller role in this setting. So, policy should shift toward investment stability and financial resilience. For example:

Macroprudential Tools:

Prioritize countercyclical capital buffers and stabilization funds to smooth the balance-sheet volatility and investment fluctuations caused by mineral price cycles.

Technological Diversification:

Success depends on increasing the "elasticity of substitution." Investment must be funneled into R&D for material efficiency and "swap-ready" chemistries such as transitioning to sodium-ion batteries or rare-earth-lean motor technologies. This allows the economy to swap chemistries as prices fluctuate, effectively muting the impact of any single mineral spike.

Financial Resilience:

Maintain precautionary wealth buffers (e.g., foreign-exchange reserves) to manage the debt-cycle impacts of mineral shocks.

Navigating the Energy Transition

The transition to minerals introduces new complexities but does not replicate the existential vulnerability of the "oil era." The economic nature of minerals as an investment component provides a natural buffer for aggregate activity.

For advanced economies, mineral price spikes are less likely than oil spikes to cause an economy-wide slump. They mainly affect investment and foreign debt. By focusing on financial stability and technological flexibility, we can manage the "wealth/user-cost shocks" of the new commodity frontier without derailing long-term growth.

Figure 1. How the economy adjusts after oil prices double versus critical mineral prices double (OECD calibration)

Notes: The solid line reports the response to an oil price doubling. The dashed line reports the response to a mineral price doubling. Values are shown relative to the initial steady-state values (pre-shock level 1.0). The horizontal axis is time after the shock. Calibration is based on OECD economy parameters.